14 Nov TOO BIG TO FAIL: FT’S LIONEL BARBER ON THE FUTURE OF FINANCIAL JOURNALISM

On Tuesday of this week, the Financial Times’ Lionel Barber announced that he would be stepping down from the position of Editor of the legacy business newspaper. In light of this news, we are sharing an article from our Innovations in News Media 2019-2020 world report. This article is the transcript of a speech given by Barber for the annual James Cameron Memorial Lecture on November 22, 2018, at City University, in London. The lecture is given in memory of the prominent British journalist. The transcript is published in our world report and below with permission and thanks.

Tonight, my point of departure is the future: the future of financial journalism.

First, the good news: the opportunities have never been greater. The internet and the giant aggregators are blamed for many sins — coarsening civic discourse, creating echo chambers, monopolising advertising revenues, influencing elections — but the digital revolution has also led to an explosion of creativity and new forms of rich storytelling.

And what stories they are: the rise and fall of corporate titans such as Sir Philip Green, the artificial intelligence revolution, peak globalisation and, lest we forget, Brexit.

Today’s business and financial journalist has never been so versatile, never so tested. On multiple platforms: print, audio, camera. They code, they compose, they collaborate in ways unimaginable a decade ago. And that’s a very good thing because quality business and financial journalism has never been more important.

Too big to fail, if you like — not only in terms of the stories but also because of their contribution to an informed shareholding democracy. The bad news is that the threats to serious financial journalism are hiding in plain sight:

• The army of public relations advisers employed by individuals and companies with thin skins and deep pockets

• ‘Black PR’ — sometimes pushed by ex-spooks — that uses social media platforms to attack and undermine reputations and independent journalism

• The rising power of private markets versus public markets, making it far harder for journalists to access information

• The encroachment of the law via gagging injunctions, non-disclosure agreements and the chilling new notion of confidentiality

• And yes, the spectre of state-sponsored regulation of the press

These are the themes, good and bad, I want to explore tonight.

First, some context and a touch of personal history. I can still remember the day I decided I wanted to be a business and financial journalist. It was the summer of 1980. Margaret Thatcher had just come to office and I was a cub reporter on the Scotsman in Edinburgh.

Keith Joseph, Mrs Thatcher’s political guru, was visiting in Glasgow and the main news desk dispatched me to cover his speech. The man dubbed by Private Eye as ‘the Mad Monk’ spoke about wealth creation and the importance of business.

Here was a great human drama of immense importance. Why was the British public and the press not interested? From that day on, I had found my calling. Sir Keith’s comments remain valid today. The creation of wealth is critical for jobs, tax revenues and a decent standard of living.

The problem in the UK is that capitalism has acquired a bad name. We are a world away from the days when Peter Mandelson could declare, with a rare straight face, that he was intensely relaxed about people becoming filthy rich, as long as they paid their taxes.

The legacy of the great crash of 2008, — economic, financial and political, — hangs heavy in the air: banks bailed out to the tune of £500 billion; the bankers responsible punished only in the court of public opinion; the imbalance between risk and sky-high rewards barely addressed by boards and shareholders.

What are we to make of the workings of modern finance and advanced economies? How should journalists respond? Well, to quote George Santayana, the Spanish philosopher and essayist, “To understand your future, you have to understand your past.”

When I joined the FT in March 1985, three institutions dominated the City of London: the Bank of England, the London Stock Exchange, and Lloyd’s of London. The pinstriped establishment exercised power in a very different way to today.

Regulation was far more informal. A gentleman’s word — and by and large they were gentlemen or, at least, men — was his bond. The Bank of England’s sanction consisted of a private audience with the governor, eyebrows raised appropriately according to the scale of the misdemeanour.

The City operated like a club. Stockbrokers and merchant banks consisted of partnerships or family-controlled advisory firms without a lot of capital. Risk-taking was tempered by the knowledge that personal fortunes were at stake.

Of course, no one is suggesting this was a foolproof system. The secondary banking crisis of 1973-1975, for example, was a monument to hubris and misjudgment of the property market.

Financial journalism was also clubby — sometimes a little too clubby for my taste. When I was a business journalist on the Sunday Times, a senior executive once gave me a piece of advice: the best way to get a good story was to wine and dine businessmen and preferably go on holiday with them too.

City editors were famously well informed about companies’ performance, often before their results went public. Some, such as Sir Patrick Sergeant of the Daily Mail, he of the matinée looks who founded Euromoney, went on to distinguished careers in business. Others, such as Patrick Hutber and Ivan Fallon of the Sunday Telegraph, were immensely influential in their time.

Everything changed with the Big Bang, which abolished fixed commissions and ending the separation of principal and agent, between the brokers and the so-called jobbers, allowing brokers to take positions which in turn led to the U.S. model of the full-service investment bank. A new age of competition followed, including foreign ownership of merchant banks and brokers.

All this amounted to a cultural revolution as much as a transformation of the financial landscape. Ruthless professionalism replaced trust as the basis of transaction. In the old days, if someone misread or misquoted a price through genuine mishap, a deal would be unwound on the basis of that trust — something inconceivable today.

Upheaval in the business of the City coincided with a revolution in the business of journalism. Technology was the driving force. It met a wall of opposition in the shape of the print trade unions, each with Orwellian acronyms like SOGAT and NATSOPA.

Two men, Eddy Shah and Rupert Murdoch, finally had the courage and the nous to take on the print unions’ monopoly on power. It ended in brutal confrontation at Wapping but ultimately a fundamental change in working practices.

The age of hot metal was over; from now on, journalists could feed their stories via computer directly to publication. The news and information technology revolution had begun — a new lease of life for newspapers and hundreds of new jobs in journalism.

There were other less noticeable changes. Pre-Big Bang, legend has it, Geoffrey Owen, then FT editor, went on his customary afternoon stroll through the newsroom. He alighted upon a markets reporter slumped across his desk.

Geoff — brow furrowed — asked if the man needed medical attention. “No sir”, came the reply, “just a long lunch gathering information”.

“Ah, that’s OK then,” said Geoffrey, “I thought he might be ill.”

London in the late 1990s and the Blairite Noughties epitomised Cool Britannia. Bigger salaries, better cuisine, cosmopolitan chic. The City ranked alongside New York as the world’s financial centre, temporarily eclipsing it after the dotcom crash.

The Thatcher-Reagan era of deregulation and globalisation — the free movement of goods, capital, labour and services — unleashed the global corporation. Along with the internet, globalisation also increased the profile and reach of business journalism.

The FT was a beneficiary, though one thing changed. The fight for scoops and talent was waged on a global stage with the Wall Street Journal, The New York Times and Bloombergrather than within the narrow confines of Fleet Street.

Business and financial journalism expanded, and so did the market power of business journalists.

Robert Thomson, Robert Peston, James Harding and Will Lewis — all FT alumni — took top jobs in the US and the BBC. Others, such as Andrew Ross Sorkin, a former New York Times reporter and now co-anchor of Squawk Box, became brands in their own right.

In the internet age, business journalism turned out to have a more robust business model than general news. Readers are wealthier and will pay for information. That’s why the FT is closing in on one million paying readers, more than three quarters of whom are subscribers.

But with this increased power and reach come four challenges:

First, stock markets have become a spectator sport, especially on cable news. Real-time commentary has supplanted in-depth sectoral coverage. The stampede for clicks has flattened reporting and dumbed down headlines. The present and future risk for publications is that they increasingly become ‘commoditised’ at speed.

These days, the half-life of a hot scoop is between five seconds and two hours. The days when the world would wake up to a world-beating financial exclusive on the front page of a newspaper are long gone.

(This is a source of acute personal regret. My all-time favourite FT scoop was a 1998 Thanksgiving story revealing the merger of oil companies Exxon and Mobil. Will Lewis’s story ruined our U.S. rivals’ turkey lunch.)

Today, news wires will follow up a scoop in a matter of seconds and then everyone will match it. Attribution appears in paragraph 11. Copyright is for pussycats.

Why?

Because in the age of Google, with its immensely powerful search algorithms, journalists can hoover up the essence of a story in seconds.

Once upon a time, we would have called this plagiarism. Now, so long as there is acknowledgement or attribution, it’s all about aggregation. The trouble is that not enough people are interested in getting out of the office and doing the legwork that, we all know, is still essential for deep and original reporting.

The second challenge is how much more powerful the private markets have become over the past decade relative to the public markets. Just think of venture capital, private equity and sovereign wealth funds and the shrinkage of public markets. Up to $1 trillion of stock buybacks a year in the U.S. alone.

Those lucky enough to have had access to these alternative investment vehicles have made huge amounts of money out of the Silicon Valley technology boom compared with retail investors. The SoftBank Vision Fund is the ultimate expression of this, as it tries to arbitrage the value between the two markets. How successfully, we shall see.

The broader point is that private companies and markets are, by definition, much more opaque and therefore difficult to report on. Holding these private companies and markets to account will be very hard. That’s why Bad Blood, John Carreyrou’s exposé on Theranos and the FT-McKinsey business book of the year, is so impressive. (It’s also worth noting that Rupert Murdoch, as a Theranos shareholder and proprietor, refused to intervene to stop or water down the story at the Wall Street Journal.)

The third challenge is the growing power of the public relations industry.

At one level, this is a roaring British success story. Sir Martin Sorrell, who — full disclosure — has featured prominently in the FT this year, built WPP into the world’s largest brand marketing and PR business. Brunswick and Finsbury are global businesses, a tribute to the ambition and drive of their founders Sir Alan Parker and Roland Rudd.

These firms see and sell themselves as much more than PR agents. They are in the ‘strategic advice’ business, almost on the same footing as the investment banker or management consultant. They crave and often win a seat at the high table, next to the CEO.

Now, gatekeepers come in all shape and sizes, from Dmitry Peskov in the Kremlin to Sarah Huckabee Sanders in the White House. They are a fact of life. My worry is the way PR is moving.

Take ‘black PR’. This year, Bell Pottinger — founded by Sir Tim Bell, one of Mrs Thatcher’s top advisers — collapsed after revelations about its ties to the corrupt Gupta business empire in South Africa.

Bell Pottinger created a bot army to target certain individuals on Twitter and other social media. Between 2016 and 2017, more than 20,000 tweets and retweets about Peter Bruce, a former colleague and distinguished national newspaper editor, were dispatched in order to discredit and humiliate. Peter’s photo appears in dozens of “lists” of enemies of the people in South Africa.

In the end, the Guptas’ attempt at state capture failed. Journalism won out. But it was a close-run thing. The same holds true of the fearless reporting of Clare Rewcastle Brown in her exposure of the multibillion-dollar 1MDB scandal in Malaysia.

Clare faced massive intimidation early on with the story before, among others, the Wall Street Journal entered the fray and blew open a story that eventually brought down the Malaysian, government led by Najib Razak.

A parallel trend is the growth of native content, often produced by PR teams, either external or in-house, often produced for advertisers or companies by the media organisations themselves. Full disclosure, that includes the FT.

Companies are “taking back control” by setting up in-house PR / social media/ “content” operations. From there, they can distribute their own “stories” on YouTube and Facebook. Similarly, Goldman Sachs hosts its own news sessions with senior executives interviewing experts in their field.

This makes it much harder to secure quality time with the CEO. Why engage with real journalists when someone browsing the web is just as likely to find your “story” when they Google your company’s name?

And finally let’s look at the growth of PR compared to the decline of newsrooms.

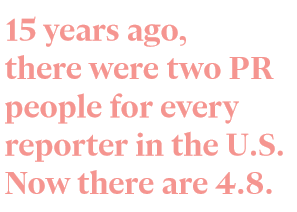

According to the U.S. Bureau of Labor Statistics, in 2000 there were 65,900 news reporters and 128,600 public relations people. In 2015: 45,800 news reporters, and 218,000 public relations people.

So, 15 years ago, there were two PR people for every reporter in the country. Now there are 4.8 PR people for every reporter.

David Simon, former Baltimore Sun staffer and creator of the HBO series ‘The Wire’ offered his own perspective on the stats.

“This is how a republic dies. Not with a bang, but a reprinted press release.”

Let me turn now to a fourth and final threat: The evolution of the law as it pertains to the practice of journalism, specifically the area covering privacy, data protection and confidentiality.

Without doubt, the internet has exacerbated privacy and data questions.

Prior to October 2000, when the Human Rights Act of 1998 came into force under Tony Blair’s government, English law did not recognise a right to privacy.

In one notorious case, a Sunday tabloid photographer snapped Gordon Kaye — the ’Allo ’Allo TV actor — in his hospital bed while recovering from brain surgery. He had no privacy protection under the law.

However, over the past 15 years or so, this area of law has developed apace. Initially, the courts stretched the equitable principles of “breach of confidence” to create something akin to a privacy right.

So, unlike Kay, the supermodel Naomi Campbell ultimately won her case against Mirror Group Newspapers in the House of Lords after she was photographed coming out of a Narcotics Anonymous meeting.

Subsequently and almost seamlessly, we have witnessed a new privacy tort of “misuse of private information” (or ‘MPI’, as lawyers refer to it.)

Editors have become used to having to weigh up competing interests of freedom of expression versus any reasonable expectation of privacy — as per articles 10 and eight respectively of the European Convention on Human Rights.

Now, the latter is not an absolute right, and it would not be so troublesome were it not for the mushrooming of data protection law, which has added to the privacy hazards facing the press. What concerns me most is the way it is being used to cover digital/online journalism, specifically via “personal data.”

Complainants are increasingly resorting to data protection law to attack or fetter journalism, with so-called ‘subject access’ requests and ‘rectification’ or ‘deletion requests.’

This position has been updated in the new UK Data Protection Act 2018, while the E.U. has passed the all-embracing General Data Protection Regulation, known as ‘GDPR’. This is already having an impact on press reporting.

In a recent case in Germany, a German banker who held a managerial position in London wished to delete his name and job title from an FT news report of a published ruling of the Central London Employment Tribunal.

The tribunal’s ruling was highly critical of his conduct in the workplace. He applied to a German court and won a temporary privacy injunction based on provisions in German law.

We are appealing against the court’s decision, as is Bloomberg. This attempt to rewrite or erase history must not be allowed to stand.

I also urge all press to argue robustly in favour of the legal exemption that is applicable to the processing of data for the “special purposes of journalism.” This is vital if we are to prevent disproportionate encroachment on journalistic freedoms through aggressive data protection claims.

Let me turn now to the “law of confidence.” As previously discussed, this law played the role of midwife in the birth of privacy law here in England.

A High Court ruling last year in the case of Brevan Howard v Reuters, which was upheld by the Court of Appeal, has reminded us all — not least in the field of business journalism — that the courts have restrictively held there is a positive public interest in maintaining obligations of confidentiality.

In order to override that, one has to show there is a pretty strong countervailing public interest in publishing the relevant “confidential” information, in order to defeat an injunction application and court claim.

We had a recent experience in the case of Guggenheim, a powerful Chicago-based investment bank that sought a temporary court injunction in the U.K. to prevent us publishing certain internal information we considered to be of considerable public interest.

Fighting the case would have entailed hundreds of thousands of pounds of legal fees. In the end, both sides agreed to terms that allowed publication of a long story on Guggenheim’s business model but without some key financial details. It was an unsatisfactory score draw.

The rise of privacy-type restrictions in the law has naturally coincided with the proliferation of online publications and digital processing. And I would remind you that the Leveson report into the newspaper industry devoted a mere 14 pages out of the 2,000 to the internet.

Today, we need to look forward — not backward — when it comes to the media, the law and potential regulation. The internet juggernauts are not merely platforms. They are publishers and should be held to the same standards.

In short, we should level the playing field.

The independence of the press — in the words of former Lord Chief Justice Igor Judge — is not a right of one section of the community. It is the right of the community as a whole. It is not only a constitutional necessity; it is a constitutional principle.

This means of course that, from time to time, the press will write terrible things and terrible headlines, like describing the judiciary as the enemies of the people.

But as Paul Dacre rightly said the other day: the press should have the freedom to get it right and the freedom to get it wrong. As an editor, I know that the freedom to make mistakes carries a heavy price.

As a financial editor, that is doubly true.

Ladies and gentlemen, I have touched on the past, and much of the present, so let me offer a sneak peek into the future. Here are three predictions.

First, the news business is on the cusp of a second technology revolution. We are rapidly approaching the moment where all text can be understood by machines — a revolution as big as the launch of the internet. Routine tasks such as writing company earnings and stock market reports will disappear.

The next AI phase will be even more profound, with speech-to-text, the processing of images and, yes, language.

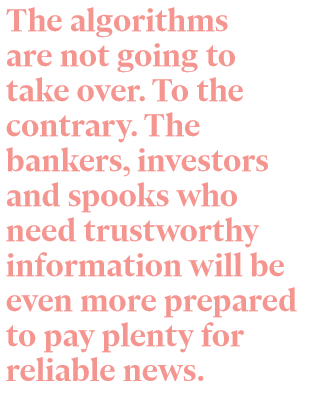

Second, the algorithms are not going to take over. To the contrary. The bankers, investors and spooks who need trustworthy information will be even more prepared to pay plenty for reliable news.

That’s why we have seen a Brexit bounce and The New York Times has witnessed a ‘Trump bump.’ And it’s why low barriers to entry will allow niche news start-ups with no legacy costs to spring up, a little like the hedge funds offering specialist knowledge after Big Bang.

Indeed, we could go back further in time to 130 years ago, when the FT was founded in the old City of London and dozens of dodgy freesheets were ramping stocks in non-existent Bolivian tin mines. Truth, so to speak, is being ‘remonetised.’

Third, and most counter-intuitively, I still believe in the value and future of print. The smart, edited snapshot of the news, with intelligent analysis and authoritative commentary. In the age of information overload, there has to be a place in the market for print, especially at the weekend.

So let’s celebrate the opportunities as well as the challenges for business and financial journalism, which is so much more than a tool for making or losing money.

It contributes to an understanding of how a modern, interconnected global economy works. It is vital for an informed citizenry.

In short: too big to fail.

This article, along with many many more is available in full, within the pages of our Innovation in News Media 2019-2020 World report, available for purchase in print or digital edition.